Most procurement decisions are made on schedule—when the contract expires, when the budget cycle forces the decision, when the order has to go out. The price on the day you have to buy is the price you pay, regardless of whether that price reflects normal market conditions or not. TSF replaces the procurement schedule with a procurement signal: a live measurement of where any price is right now relative to its own structural baseline. When the signal fires, the price is abnormally low. That’s when you buy.

Stock Market: TSF publishes a specific limit order price for each stock every Sunday, one week in advance. That price is not a prediction: it is the price at which the stock is structurally cheap relative to its own baseline. During the trading week, if the stock's intraday low hits that price, the signal fires. Validation across thousands of live trades shows an 80% probability of profitability within 120 days. The same methodology applies to any price series, including freight rates, energy contracts, commodities, identifying the specific price level at which procurement is measurably cheap and signaling when the market hits it.

Freight and Logistics: Spot freight rates move in structural patterns. When rates fall below their structural baseline, capacity is abnormally cheap. That is the window to lock contracts, forward-book lanes, or shift volume to spot before the market corrects.

Energy Planning: Fuel, electricity, and commodity energy prices have structural baselines that reflect normal supply and demand conditions. When spot prices fall below that baseline, the cost of energy is abnormally low. That is the signal to execute forward contracts or accelerate procurement—not when the need arises, but when the price is right.

Procurement Signals Use Market Pricing Data

Procurement timing signals are built entirely from public market data. Every price series including equities, freight indices, energy benchmarks, and commodity spot prices is publicly available, continuously updated, and structurally forecastable using the TSF methodology. No proprietary data feeds, no client data connections, and no historical data onboarding are required. The signal is generated from the public market record alone.

Procurement timing is delivered as a licensed signal subscription. TSF publishes the structural baseline and confidence bands for any price series on a weekly basis. When the market price hits the lower confidence band, the price is abnormally low. The subscriber acts. TSFStocks.com demonstrates exactly how this works: weekly limit order prices published in advance for individual equities, with every historical signal and outcome publicly visible and independently verifiable.

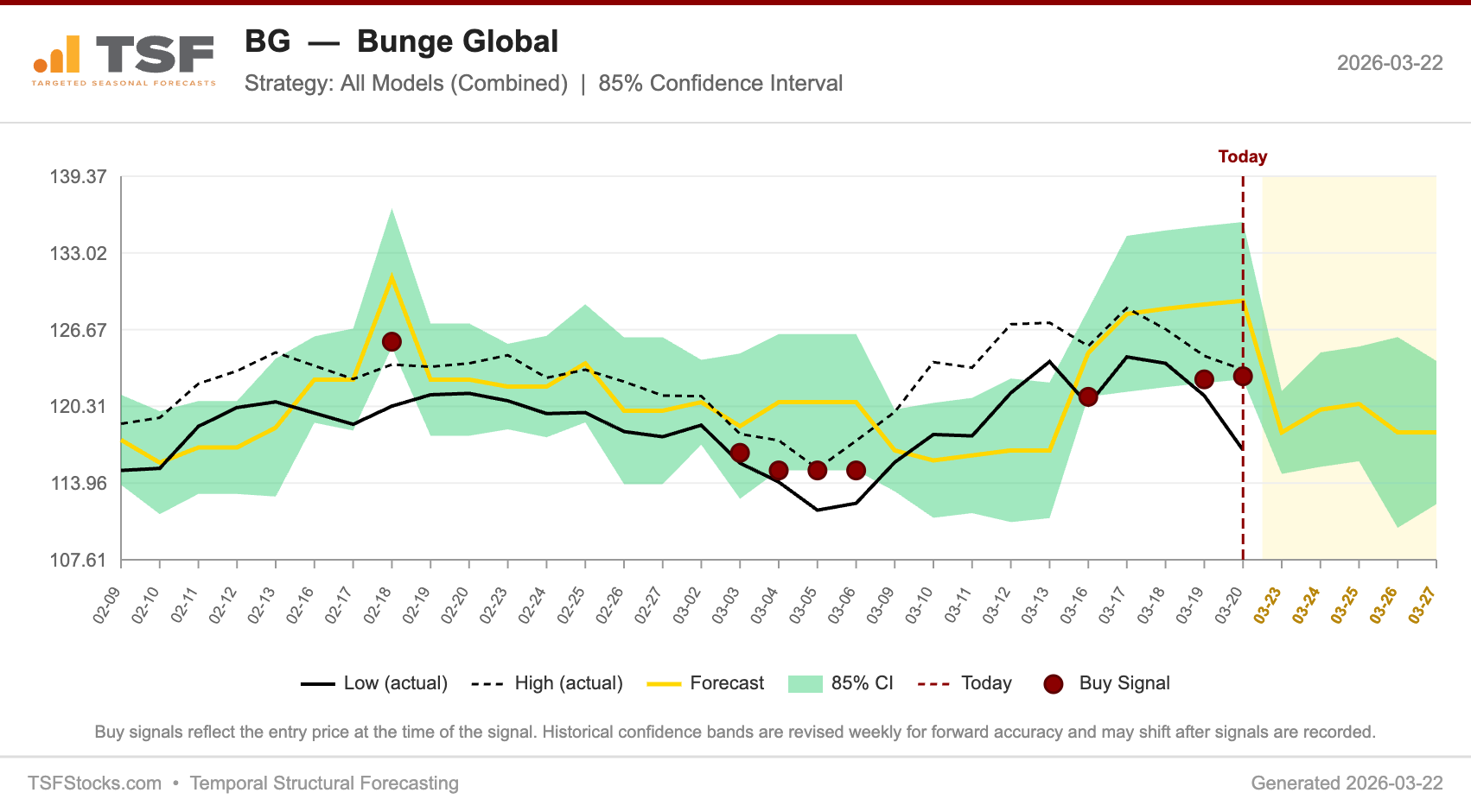

The forecast chart pictured below illustrates how this process works.

Forecasts for each entity are generated one week in advance. The lower band values represent the target procurement prices. With stocks, these can be placed as buy limit orders that fill if and when the live intraday price drops to that value. The red dots in the chart show dates when the buy signal fired. Note that the buy signals represent an optimal purchase price, not the best possible purchase price: the actual low price each day may be lower than the purchase price, but it's not possible to know what the actual low price will be in advance. TSF Demand lets you identify a target purchase price for each day, one week in advance.

The dashboard example is a live page from TSFStocks.com with the current top-ranked swing trade stock picks.

Explore the TSF Stocks Swing Trade Dashboard →

See What TSF Demand Can Do For Your Business

Every TSF Demand engagement starts with a free consultation. We review your data environment, walk through your planning needs, and give you a clear picture of what the service would look like for your business. You decide what happens next.